Page 140 - annual_report_2024

P. 140

138 CA Sri Lanka Integrated Annual Report 2024

Notes to the Financial Statements Contd.

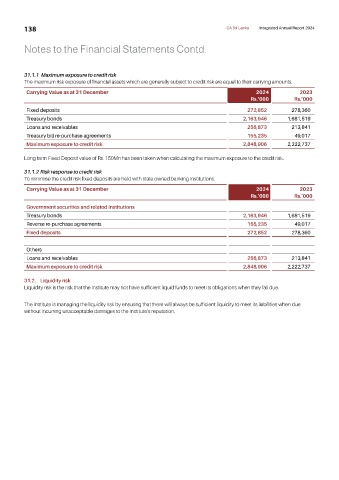

31.1.1 Maximum exposure to credit risk

The maximum risk exposure of financial assets which are generally subject to credit risk are equal to their carrying amounts.

Carrying Value as at 31 December 2024 2023

Rs.’000 Rs.’000

Fixed deposits 272,852 278,360

Treasury bonds 2,163,946 1,681,519

Loans and receivables 256,873 213,841

Treasury bill re-purchase agreements 155,235 49,017

Maximum exposure to credit risk 2,848,906 2,222,737

Long term Fixed Deposit value of Rs. 150Mn has been taken when calculating the maximum exposure to the credit risk.

31.1.2 Risk response to credit risk

To minimise the credit risk fixed deposits are held with state owned banking institutions.

Carrying Value as at 31 December 2024 2023

Rs.’000 Rs.’000

Government securities and related institutions

Treasury bonds 2,163,946 1,681,519

Reverse re-purchase agreements 155,235 49,017

Fixed deposits 272,852 278,360

Others

Loans and receivables 256,873 213,841

Maximum exposure to credit risk 2,848,906 2,222,737

31.2. Liquidity risk

Liquidity risk is the risk that the Institute may not have sufficient liquid funds to meet its obligations when they fall due.

The Institute is managing the liquidity risk by ensuring that there will always be sufficient liquidity to meet its liabilities when due

without incurring unacceptable damages to the Institute’s reputation.