Page 135 - annual_report_2024

P. 135

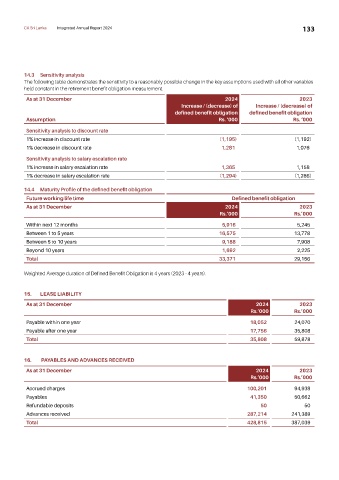

CA Sri Lanka Integrated Annual Report 2024 133

14.3 Sensitivity analysis

The following table demonstrates the sensitivity to a reasonably possible change in the key assumptions used with all other variables

held constant in the retirement benefit obligation measurement.

As at 31 December 2024 2023

Increase / (decrease) of Increase / (decrease) of

defined benefit obligation defined benefit obligation

Assumption Rs. ‘000 Rs. ‘000

Sensitivity analysis to discount rate

1% increase in discount rate (1,195) (1,192)

1% decrease in discount rate 1,281 1,076

Sensitivity analysis to salary escalation rate

1% increase in salary escalation rate 1,365 1,158

1% decrease in salary escalation rate (1,294) (1,286)

14.4 Maturity Profile of the defined benefit obligation

Future working life time Defined benefit obligation

As at 31 December 2024 2023

Rs.’000 Rs.’000

Within next 12 months 5,916 5,245

Between 1 to 5 years 16,575 13,778

Between 5 to 10 years 9,188 7,908

Beyond 10 years 1,692 2,225

Total 33,371 29,156

Weighted Average duration of Defined Benefit Obligation is 4 years (2023 - 4 years).

15. LEASE LIABILITY

As at 31 December 2024 2023

Rs.’000 Rs.’000

Payable within one year 18,052 24,070

Payable after one year 17,756 35,808

Total 35,808 59,878

16. PAYABLES AND ADVANCES RECEIVED

As at 31 December 2024 2023

Rs.’000 Rs.’000

Accrued charges 100,201 94,938

Payables 41,350 50,662

Refundable deposits 50 50

Advances received 287,214 241,389

Total 428,815 387,039