Page 134 - annual_report_2024

P. 134

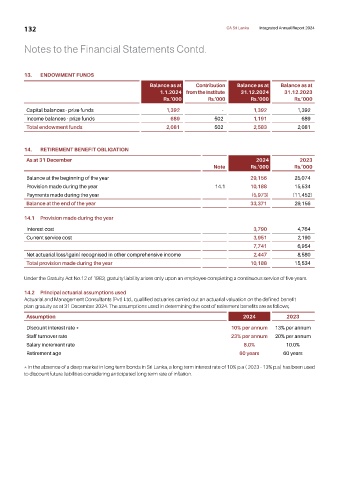

132 CA Sri Lanka Integrated Annual Report 2024

Notes to the Financial Statements Contd.

13. ENDOWMENT FUNDS

Balance as at Contribution Balance as at Balance as at

1.1.2024 from the Institute 31.12.2024 31.12.2023

Rs.’000 Rs.’000 Rs.’000 Rs.’000

Capital balances - prize funds 1,392 - 1,392 1,392

Income balances - prize funds 689 502 1,191 689

Total endowment funds 2,081 502 2,583 2,081

14. RETIREMENT BENEFIT OBLIGATION

As at 31 December 2024 2023

Note Rs.’000 Rs.’000

Balance at the beginning of the year 29,156 25,074

Provision made during the year 14.1 10,188 15,534

Payments made during the year (5,973) (11,452)

Balance at the end of the year 33,371 29,156

14.1 Provision made during the year

Interest cost 3,790 4,764

Current service cost 3,951 2,190

7,741 6,954

Net actuarial loss/(gain) recognised in other comprehensive income 2,447 8,580

Total provision made during the year 10,188 15,534

Under the Gratuity Act No.12 of 1983, gratuity liability arises only upon an employee completing a continuous service of five years.

14.2 Principal actuarial assumptions used

Actuarial and Management Consultants (Pvt) Ltd., qualified actuaries carried out an actuarial valuation on the defined benefit

plan-gratuity as at 31 December 2024. The assumptions used in determining the cost of retirement benefits are as follows,

Assumption 2024 2023

Discount interest rate * 10% per annum 13% per annum

Staff turnover rate 23% per annum 20% per annum

Salary increment rate 8.0% 10.0%

Retirement age 60 years 60 years

* In the absence of a deep market in long term bonds in Sri Lanka, a long term interest rate of 10% p.a ( 2023 - 13% p.a) has been used

to discount future liabilities considering anticipated long term rate of inflation.