Page 141 - annual_report_2024

P. 141

CA Sri Lanka Integrated Annual Report 2024 139

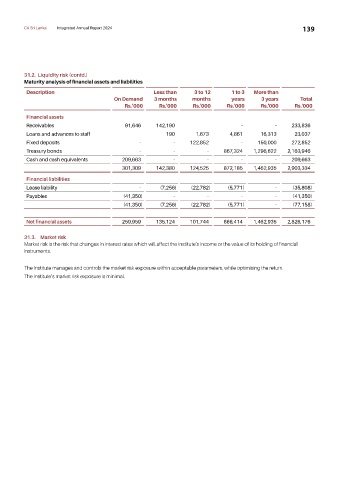

31.2. Liquidity risk (contd.)

Maturity analysis of financial assets and liabilities

Description Less than 3 to 12 1 to 3 More than

On Demand 3 months months years 3 years Total

Rs.’000 Rs.'000 Rs.'000 Rs.'000 Rs.'000 Rs.'000

Financial assets

Receivables 91,646 142,190 - - 233,836

Loans and advances to staff 190 1,673 4,861 16,313 23,037

Fixed deposits - - 122,852 - 150,000 272,852

Treasury bonds - - - 867,324 1,296,622 2,163,946

Cash and cash equivalents 209,663 - - - - 209,663

301,309 142,380 124,525 872,185 1,462,935 2,903,334

Financial liabilities

Lease liability - (7,256) (22,782) (5,771) - (35,808)

Payables (41,350) - - - - (41,350)

(41,350) (7,256) (22,782) (5,771) - (77,158)

Net financial assets 259,959 135,124 101,744 866,414 1,462,935 2,826,176

31.3. Market risk

Market risk is the risk that changes in interest rates which will affect the Institute’s income or the value of its holding of financial

instruments.

The Institute manages and controls the market risk exposure within acceptable parameters, while optimising the return.

The Institute’s market risk exposure is minimal.