Page 125 - annual_report_2024

P. 125

CA Sri Lanka Integrated Annual Report 2024 123

(b) Other Income

The sources of other income are recognised as per the Conceptual Framework and other applicable standards. The following table

provides the details of sources of other income along with the treatment being followed.

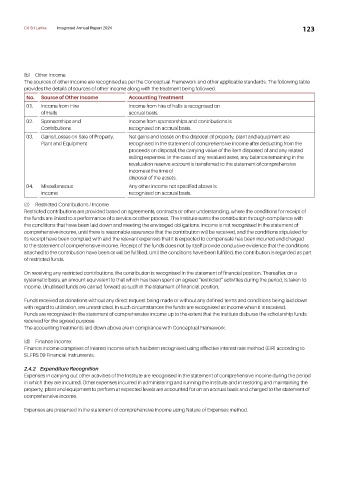

No. Source of Other Income Accounting Treatment

01. Income from Hire Income from hire of halls is recognised on

of Halls accrual basis.

02. Sponsorships and Income from sponsorships and contributions is

Contributions recognised on accrual basis.

03. Gains/Losses on Sale of Property, Net gains and losses on the disposal of property, plant and equipment are

Plant and Equipment recognised in the statement of comprehensive income after deducting from the

proceeds on disposal, the carrying value of the item disposed of and any related

selling expenses. In the case of any revalued asset, any balance remaining in the

revaluation reserve account is transferred to the statement of comprehensive

income at the time of

disposal of the assets.

04. Miscellaneous Any other income not specified above is

Income recognised on accrual basis.

(c) Restricted Contributions / Income

Restricted contributions are provided based on agreements, contracts or other understanding, where the conditions for receipt of

the funds are linked to a performance of a service or other process. The Institute earns the contribution through compliance with

the conditions that have been laid down and meeting the envisaged obligations. Income is not recognised in the statement of

comprehensive income, until there is reasonable assurance that the contribution will be received, and the conditions stipulated for

its receipt have been complied with and the relevant expenses that it is expected to compensate has been incurred and charged

to the statement of comprehensive income. Receipt of the funds does not by itself provide conclusive evidence that the conditions

attached to the contribution have been or will be fulfilled. Until the conditions have been fulfilled, the contribution is regarded as part

of restricted funds.

On receiving any restricted contributions, the contribution is recognised in the statement of financial position. Thereafter, on a

systematic basis, an amount equivalent to that which has been spent on agreed “restricted” activities during the period, is taken to

income. Unutilised funds are carried forward as such in the statement of financial position.

Funds received as donations without any direct request being made or without any defined terms and conditions being laid down

with regard to utilisation, are unrestricted. In such circumstances the funds are recognised as income when it is received.

Funds are recognized in the statement of comprehensive income up to the extent that the Institute disburse the scholarship funds

received for the agreed purpose.

The accounting treatments laid down above are in compliance with Conceptual Framework.

(d) Finance Income:

Finance income comprises of Interest income which has been recognised using effective interest rate method (EIR) according to

SLFRS 09 Financial Instruments.

2.4.2 Expenditure Recognition

Expenses in carrying out other activities of the Institute are recognised in the statement of comprehensive income during the period

in which they are incurred. Other expenses incurred in administering and running the Institute and in restoring and maintaining the

property, plant and equipment to perform at expected levels are accounted for on an accrual basis and charged to the statement of

comprehensive income.

Expenses are presented in the statement of comprehensive income using Nature of Expenses method.