Page 123 - annual_report_2024

P. 123

CA Sri Lanka Integrated Annual Report 2024 121

2.3.3 Endowment Funds

Where assets are received as an endowment, which are not exhausted, only the income earned from such assets may be recognized

and used as income.

Investment income and other gains realized from funds available under each of the above categories are allocated to the appropriate

funds, unless the relevant agreement or minute provides otherwise.

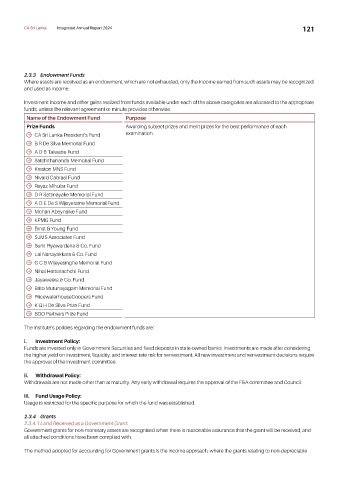

Name of the Endowment Fund Purpose

Prize Funds Awarding subject prizes and merit prizes for the best performance of each

E CA Sri Lanka President’s Fund examination.

E B R De Silva Memorial Fund

E A D B Talwatte Fund

E Satchithananda Memorial Fund

E Kreston MNS Fund

E Nivard Cabraal Fund

E Reyaz Mihular Fund

E D R Settinayake Memorial Fund

E A D E De S Wijeyeratne Memorial Fund

E Mohan Abeynaike Fund

E KPMG Fund

E Ernst & Young Fund

E SJMS Associates Fund

E Sunil Piyawardena & Co. Fund

E Lal Nanayakkara & Co. Fund

E G C B Wijeyesinghe Memorial Fund

E Nihal Hettiarachchi Fund

E Jayaweera & Co. Fund

E Brito Mutunayagam Memorial Fund

E PricewaterhouseCoopers Fund

E K G H De Silva Prize Fund

E BDO Partners Prize Fund

The Institute’s policies regarding the endowment funds are:

i. Investment Policy:

Funds are invested only in Government Securities and fixed deposits in state owned banks. Investments are made after considering

the higher yield on investment, liquidity, and interest rate risk for reinvestment. All new investment and reinvestment decisions require

the approval of the investment committee.

ii. Withdrawal Policy:

Withdrawals are not made other than at maturity. Any early withdrawal requires the approval of the F&A committee and Council.

iii. Fund Usage Policy:

Usage is restricted for the specific purpose for which the fund was established.

2.3.4 Grants

2.3.4.1 Land Received as a Government Grant:

Government grants for non-monetary assets are recognised when there is reasonable assurance that the grant will be received, and

all attached conditions have been complied with.

The method adopted for accounting for Government grants is the income approach, where the grants relating to non-depreciable