Page 117 - annual_report_2024

P. 117

CA Sri Lanka Integrated Annual Report 2024 115

their responsibility for the financial effects on the amounts recognised in the (b) Depreciation

statements and financial statements were financial statements is as follows. Depreciation is calculated by using a

approved and authorised for issue by straight-line method on the cost of all

the Council at the meeting held on 27th (a) Defined Benefit Plans property, plant and equipment, in order to

March 2025. The cost of the defined benefit plan of write-off such amounts over the estimated

employees is determined using Projected useful life of such assets.

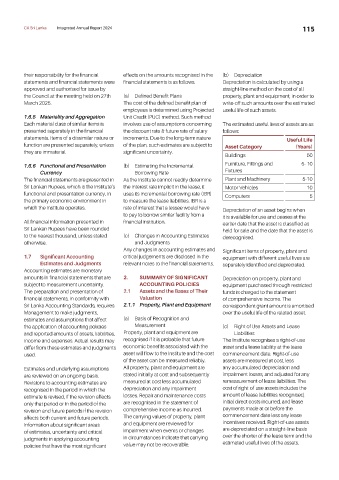

1.6.5 Materiality and Aggregation Unit Credit (PUC) method. Such method

Each material class of similar items is involves use of assumptions concerning The estimated useful lives of assets are as

presented separately in the financial the discount rate & future rate of salary follows:

statements. Items of a dissimilar nature or increments. Due to the long-term nature Useful Life

function are presented separately, unless of the plan, such estimates are subject to Asset Category (Years)

they are immaterial. significant uncertainty.

Buildings 50

1.6.6 Functional and Presentation (b) Estimating the Incremental Furniture, Fittings and 5- 10

Currency Borrowing Rate Fixtures

The financial statements are presented in As the Institute cannot readily determine Plant and Machinery 5-10

Sri Lankan Rupees, which is the Institute’s the interest rate implicit in the lease, it Motor Vehicles 10

functional and presentation currency, in uses its incremental borrowing rate (IBR) Computers 5

the primary economic environment in to measure the lease liabilities. IBR is a

which the Institute operates. rate of interest that a lessee would have Depreciation of an asset begins when

to pay to borrow similar facility from a it is available for use and ceases at the

All financial information presented in financial institution. earlier date that the asset is classified as

Sri Lankan Rupees have been rounded held for sale and the date that the asset is

to the nearest thousand, unless stated (c) Changes in Accounting Estimates derecognised.

otherwise. and Judgments

Any changes in accounting estimates and Significant items of property, plant and

1.7 Significant Accounting critical judgements are disclosed in the equipment with different useful lives are

Estimates and Judgments relevant notes to the financial statements. separately identified and depreciated.

Accounting estimates are monetary

amounts in financial statements that are 2. SUMMARY OF SIGNIFICANT Depreciation on property, plant and

subject to measurement uncertainty. ACCOUNTING POLICIES equipment purchased through restricted

The preparation and presentation of 2.1 Assets and the Bases of Their funds is charged to the statement

financial statements, in conformity with Valuation of comprehensive income. The

Sri Lanka Accounting Standards, requires 2.1.1 Property, Plant and Equipment correspondent grant amount is amortised

Management to make judgments, over the useful life of the related asset.

estimates and assumptions that affect (a) Basis of Recognition and

the application of accounting policies Measurement (c) Right of Use Assets and Lease

and reported amounts of assets, liabilities, Property, plant and equipment are Liabilities

income and expenses. Actual results may recognised if it is probable that future The Institute recognises a right-of-use

differ from these estimates and judgments economic benefits associated with the asset and a lease liability at the lease

used. asset will flow to the Institute and the cost commencement date. Right-of-use

of the asset can be measured reliably. assets are measured at cost, less

Estimates and underlying assumptions All property, plant and equipment are any accumulated depreciation and

are reviewed on an ongoing basis. stated initially at cost and subsequently impairment losses, and adjusted for any

Revisions to accounting estimates are measured at cost less accumulated remeasurement of lease liabilities. The

recognised in the period in which the depreciation and any impairment cost of right-of-use assets includes the

estimate is revised, if the revision affects losses. Repair and maintenance costs amount of lease liabilities recognised,

only that period or in the period of the are recognised in the statement of initial direct costs incurred, and lease

revision and future periods if the revision comprehensive income as incurred. payments made at or before the

affects both current and future periods. The carrying values of property, plant commencement date less any lease

Information about significant areas and equipment are reviewed for incentives received. Right-of-use assets

of estimates, uncertainty and critical impairment when events or changes are depreciated on a straight-line basis

judgments in applying accounting in circumstances indicate that carrying over the shorter of the lease term and the

estimated useful lives of the assets.

policies that have the most significant value may not be recoverable.